1.1 What is economics?

Economics as a social science

Economics = social science, because:

•

It deals with human society and behavior(how societies organize their activities,how they behave to meet their needs and wants)

•

Its approach to studying human society is based on the scientific method.

Due to the complexities within societies, economists build models so as to better understand certain interactions

•

A model is a simplified version of reality

•

All models make a range of assumptions. These are often generalized on behaviors, choices and outcomes

9 Central concepts

Scarcity | Excess of human wants over what can actually be produced to fulfill these wants

• People have unlimited wants but resources are limited

• All needs and wants can’t be satisfied; this necessitates choices and give rise to the idea of opportunity costs |

Choice | Since resources are scarce, not all needs and wants can be satisfied → choices must be made |

Efficiency | Making the best possible use of scarce resources to produce the combinations of goods and services that are optimum for society → minimize resource waste.

• Allocative efficiency refers to making the best possible use of these resources that is optimum for society = minimizing resource waste |

Equity | Idea of fairness |

Economic well-being | Quality of living standards enjoyed by members of an economy. Multifaceted concept encompassing prosperity, quality of life, financial security, and freedom of choice. |

Sustainability | Ability of the present generation to meet its needs without compromising the ability of future generations to meet their needs. |

Change | World that is studied by economists is always subject to continuous and profound change at institutional, structural, technological, economic and social levels. |

Interdependence | Economic agents such as consumers, firms, households, workers and governments interact with each other to achieve economic goals. Therefore, any action of economic agents will impact other agents. |

Intervention | Government involvement in the workings of markets. |

The problem of scarcity and choice

The basic economic problem is that resources are scarce

In economics, these resources are called the factors of production

There are finite resources available in relation to the infinite wants and needs that humans have

Needs are essential to human life e.g. shelter, food, clothing

Wants are non-essential desires e.g. better housing, a yacht etc.

Scarcity:

excess of human wants over what can actually be produced to fulfill these wants.

Resources (factors of production)

Land | Everything grown or extracted from land or sea. (e.g. forests, fish,crops) |

Labour | Human input, both physical and mental, into production. |

Capital | Man-made resources that help to produce other goods and services. |

Entrepreneurship | Person who combines the factors of production to start a business. |

Opportunity cost

Opportunity cost:benefit lost from the next (second) best alternative given up when making a decision.

Economic goods | Free goods |

Goods that require scarce resources to be sacrificed → opportunity cost (e.g. oil and iPhones) | Goods that do not require scarce resources to be sacrificed → zero opportunity cost (e.g. air, sunlight, webpages) |

The basic economic questions

1.

What should be produced?

2.

How should it be produced?

3.

For whom should it be produced?

Stakeholders in an Economy

Consumers | Producers | Workers | Government |

Scarcity has a direct influence on price

Scarcer a resource= high price | Scarce resource = higher cost of production | Employers may not have the resources to create a safer working environment | Decide whether goods can be provided by private firms or public

Influences allocation of resources |

Economic systems

Free market economy | Command economy | Mixed economy |

Resources are owned by private individuals | Resources are owned by the government (or the public sector) | Resources are owned by both the private and public sectors. |

Economic Goods & Free Goods

Economic goods are scarce in relation to the demand for them

•

Due to valuability = producers attempt to supply to generate profit

•

E.g. Oil, corn, gold

Free goods are abundant in supply

•

Unable to profit from supplying free goods

•

E.g. sunlight, air, sea water

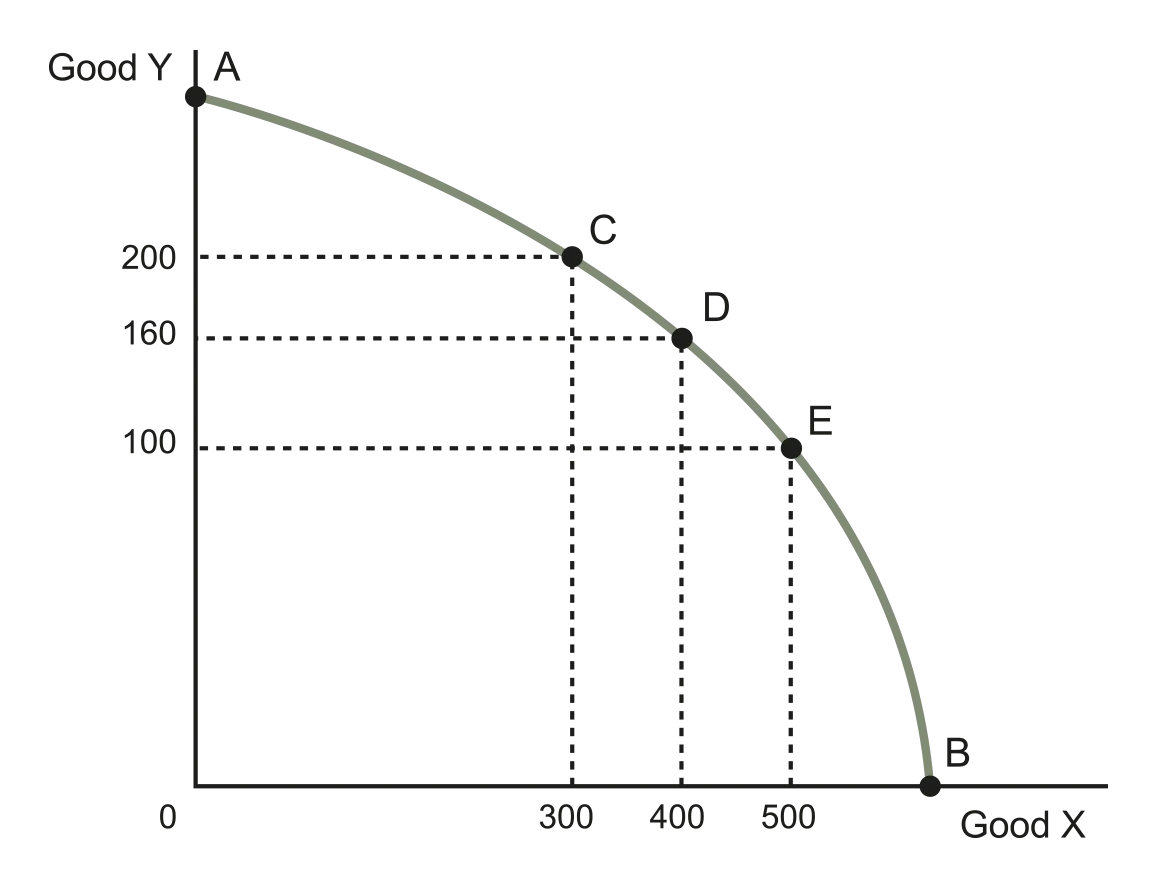

The production possibilities curve (PPC) model

Production possibilities curve (PPC): a model that shows the maximum output of 2 goods or services that can be produced by an economy if all resources are used efficiently.

Assumptions of the model

•

The economy produces only 2 goods.

•

All the resources in the economy are fully employed.

•

The resources and state of technology are fixed.

Figure 1.1.1 Production possibilities curve

Choice, opportunity cost and scarcity

PPCs demonstrate the concept of choice and opportunity cost.

•

Choice to produce at a different point on the PPC(e.g. C → D) → produce more of one good but the opportunity cost will be how much of the other good

Negative slope of PPC

•

Scarcity requires that producing more of one good necessitates producing less of the other

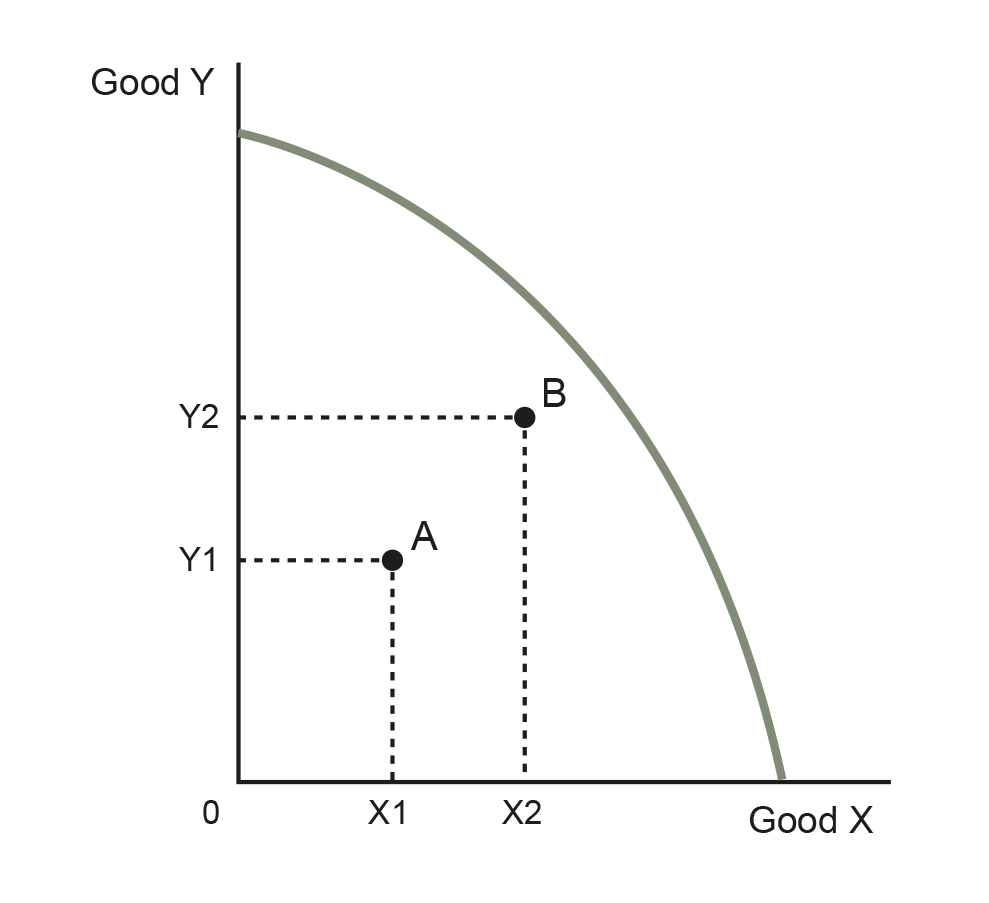

Actual growth

Figure 1.1.2 Actual growth

•

Point A: available resources not being fully utilised (e.g. unemployment) = inefficient production combination.

•

Point B: lower unemployment, more efficient use of existing resources.

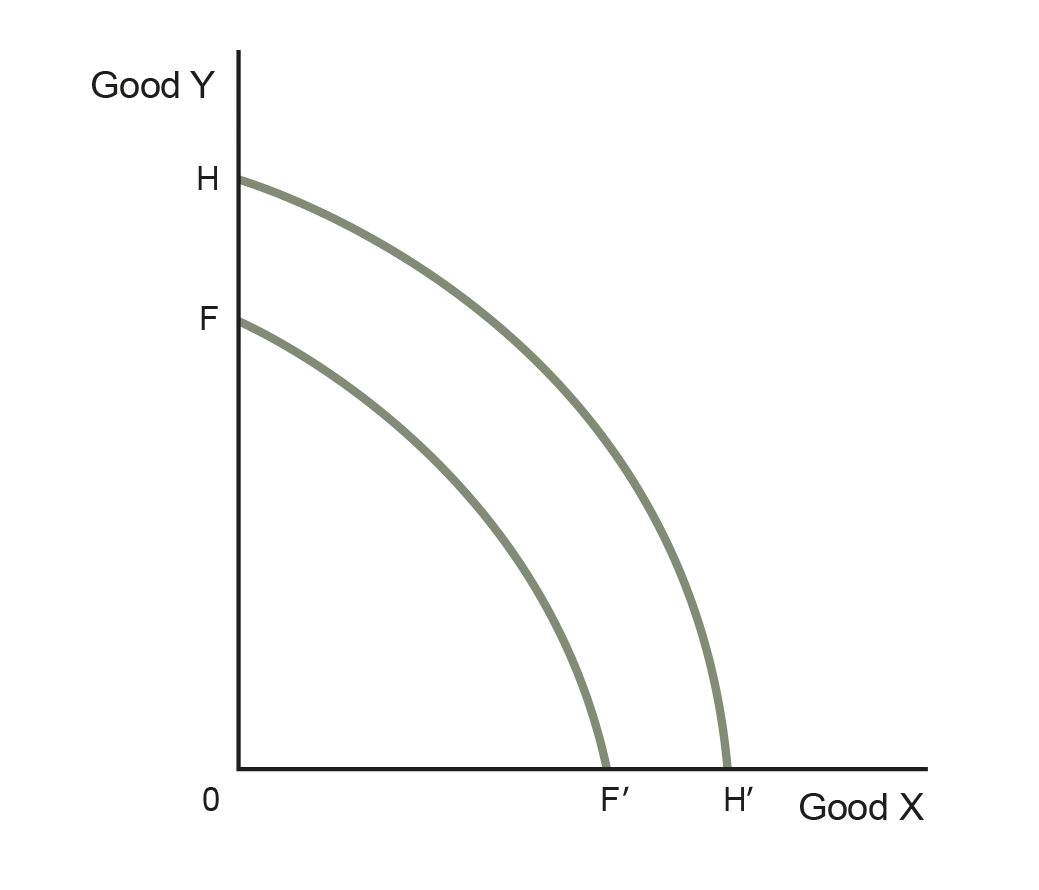

Potential growth

Figure 1.1.3 Potential growth

•

PPC shifts outwards → the economy produces combinations of Good X and Good Y that were previously unattainable.

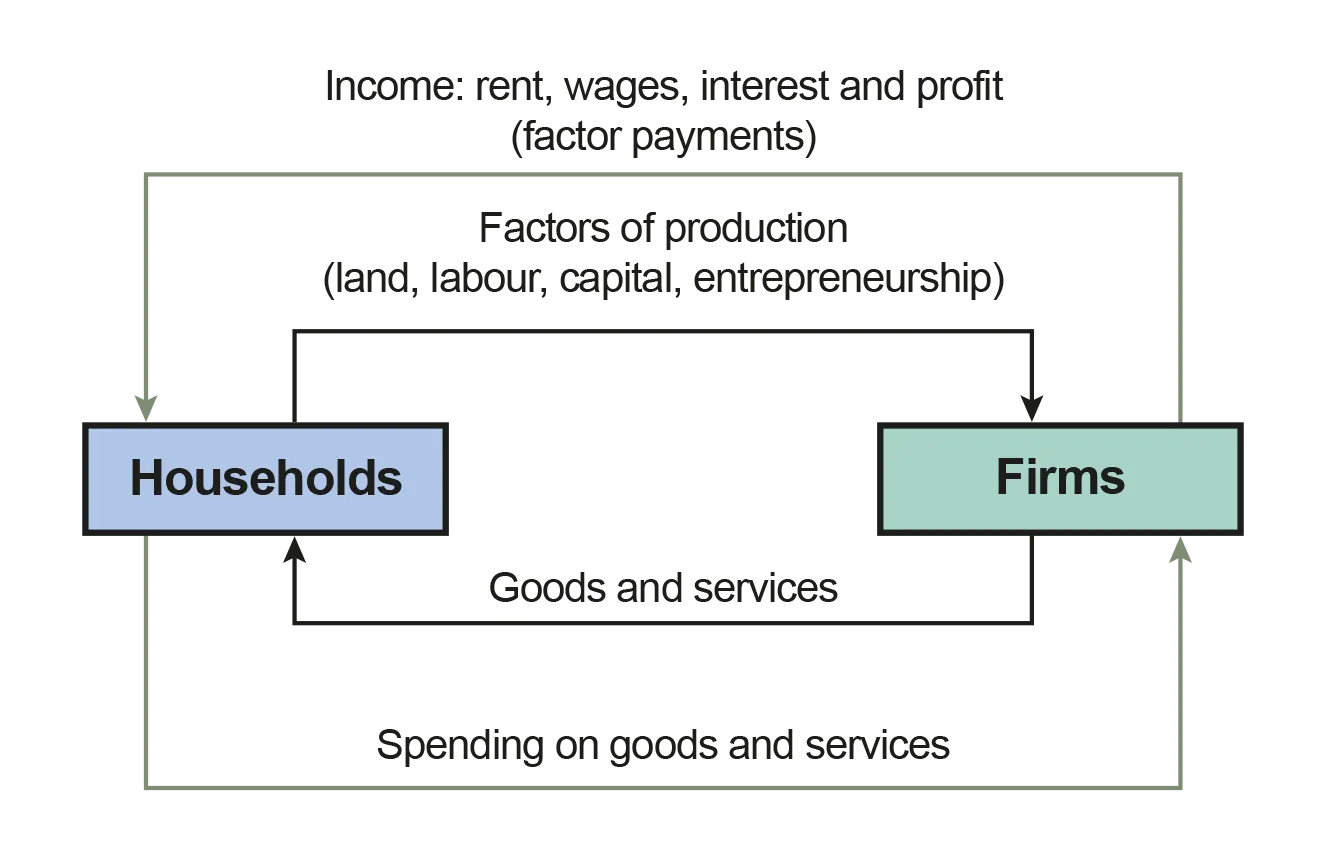

Modeling the economy

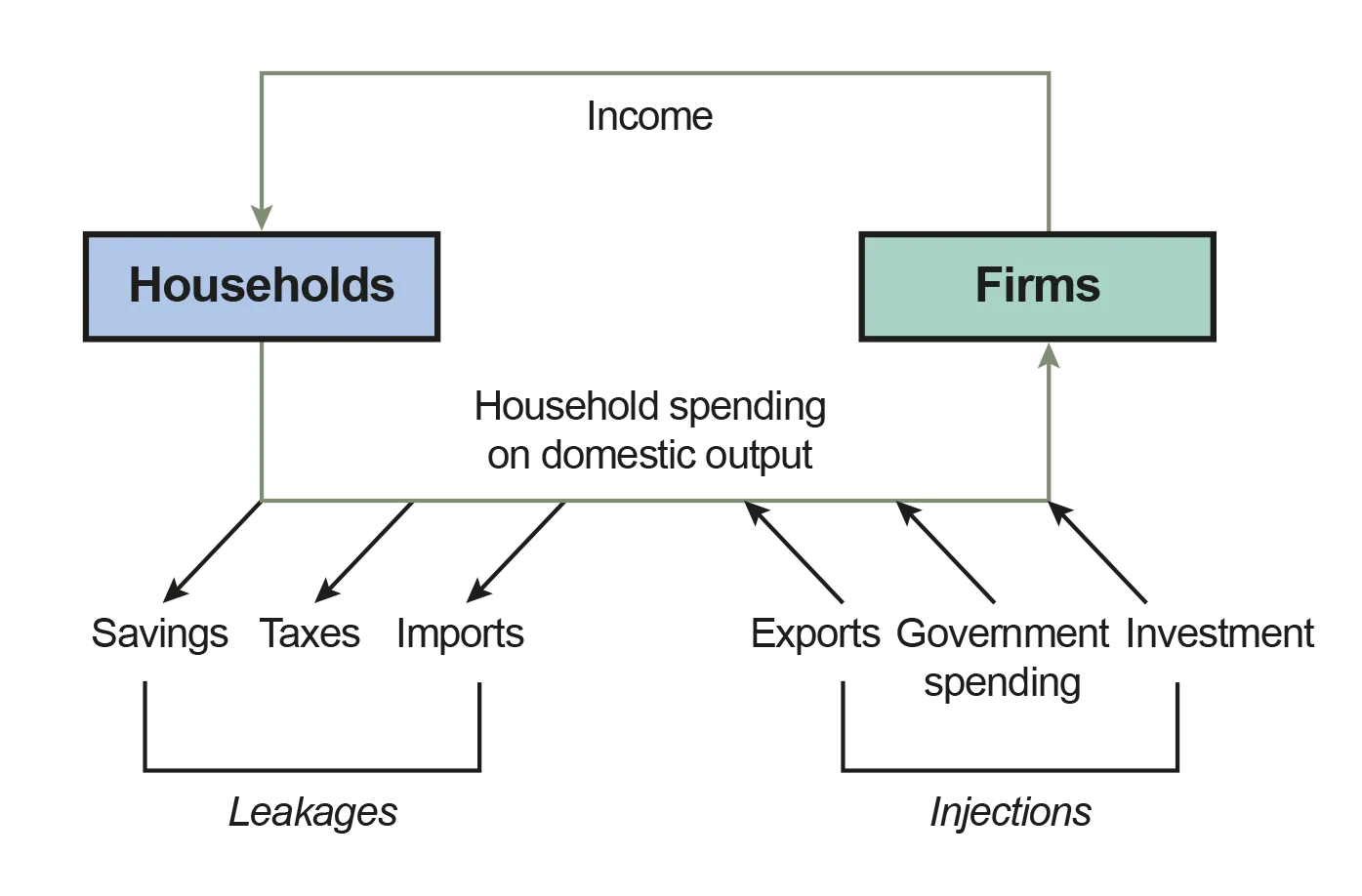

The circular flow of income model

Circular flow:

the way in which income flows around the economy, from firms to households and back to firms in a continuous process in a closed economy.

Figure 1.1.4 Circular flow of income

Factors of production | Factor payments |

Land | Rent |

Labour | Wages |

Capital | Interest |

Entrepreneurship | Profit |

Figure 1.1.5 Leakages and injections in the circular flow of income

Leakages from the circular flow | Injections into the circular flow |

• Savings

• Taxation

• Imports | • Export

• Government spending

• Investment |

1.2 How do economists approach the world?

Economic methodology

The role of positive economics

Positive economics: tries to describe, explain, and predict economic events by using hypotheses, theories and models.

Use of logic | Use of hypotheses | Empirical evidence |

Economists use careful reasoning to draw out potential implications. | Economists make general hypotheses about the causes of economic phenomena. | Once a hypothesis has been formulated it can then be tested against empirical evidence. |

The role of normative economics

Normative economics: deals with how things in the economy should or ought to be based on beliefs or value judgments about what should happen, what is good or bad, what is right or wrong.

Value judgments | Meaning of equity and equality |

Advise policymakers on which policies to pursue depending on the issues faced. | Equitable ≠ equal Equitable = fair: fairness means different things to different people → equity is a normative concept. |

Economic thought

18th century: Adam Smith

Adam Smith’s contribution to economics:

•

Laissez-faire.

•

The invisible hand.

•

Specialization, trade and wealth creation.

Laissez-faire | The invisible hand | Specialization, trade and wealth creation |

If firms want to attract customers, they must produce quality goods at competitive prices. → no need for government intervention. | When private producers are left alone to decide what to produce and how to produce, they are guided by an ‘invisible hand’. They are not told what to produce by a government or any other authority. | Increase productivity and therefore a firm’s output and profit, a worker’s wage and ultimately the wealth of the nation. |

19th century

Jean-Baptiste Say’s law: supply creates its own demand.

•

Because of the circular flow nature of a closed economy, spending cannot fall enough to prevent all the output produced from being bought.

•

Firms produce goods and services (supply) & pay households for providing them with the resources for producing the output.

•

Households receive this income and spend (demand) it to buy goods and services.

Marxist critique of classical economic thought

Capitalism exploits workers | Capitalism is innately unstable |

Actually, price paid for a good > value of labor put into producing it.

The factory owners had an incentive to pay workers as little as possible: force workers to work under appalling conditions → owners maximize profits. | Competition would force capitalists to keep investing in new machinery to reduce labor costs.

→ workers unemployed and poverty- stricken.

→ reduces the profits for factory owners. |

20th century

John Maynard Keynes

•

In a recession, wages were ‘sticky’ downwards: wages couldn’t fall easily.

◦

Sticky wages = sticky prices: producers couldn’t lower their prices if they had to go on paying the same levels of wages.

•

Falling wages meant that workers would have less money to spend, which would cause overall demand and spending to fall.

•

As a result, the economic system couldn’t return to full employment on its own.

21st century

Behavioral economics: questions the idea that marginal utility underlies demand and rational consumer behavior.

•

Consumers do not have the necessary information available to make optimal decisions.

•

Human mind works in ways that are not rational in the ways the theory presupposes.

Circular economy: a more efficient and environmentally sound alternative to the traditional linear economy.

•

Keep resources in use for as long as possible, extract the maximum value from them whilst in use, and then recover and regenerate products at the end of their life.