Aggregate demand

Aggregate demand(AD): total spending on domestic goods and services at average price levels per period of time.

•

AD = C + I + G + (X-M)

◦

C = consumption expenditures

◦

I = investment expenditures

◦

G = government expenditures

◦

X-M = net export (export - import)

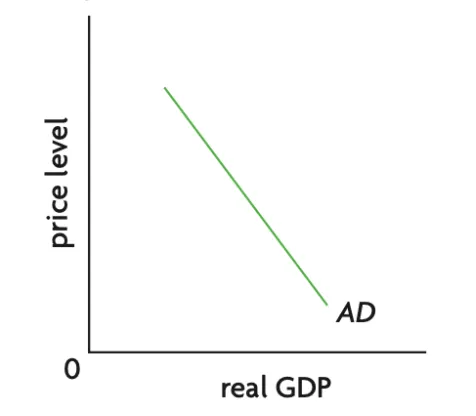

Figure 3.2.1 The aggregate demand curve

Why is the AD curve downward sloping?

Wealth effect | Trade effect | Interest rate effect |

average price level(APL) ↑ → real value of money people possess ↓ (i.e. people feel ‘poorer’) → consumer expenditure (C) ↓ → C is a component of AD → upward movement along AD | APL ↑ → exports become less competitive abroad // imports seem more attractive at home country → value of net export (X-M) ↓ → X-M is component of AD → upward movement along AD . | APL ↑ → demand for holding money ↑ → C and investment expenditure (I) ↓

(i.e. people and firms will borrow less from banks to buy durables and capital equipment) → C & I are components of AD → upward movement along AD . |

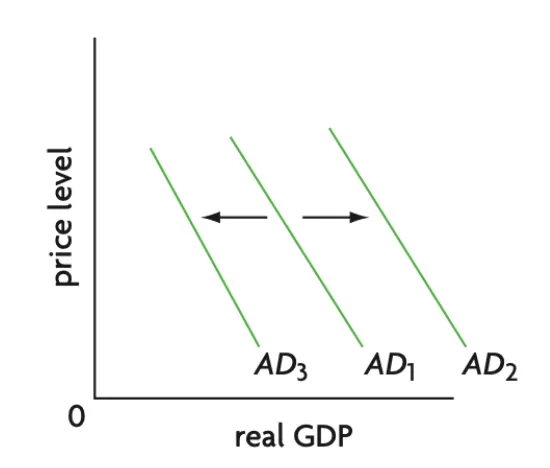

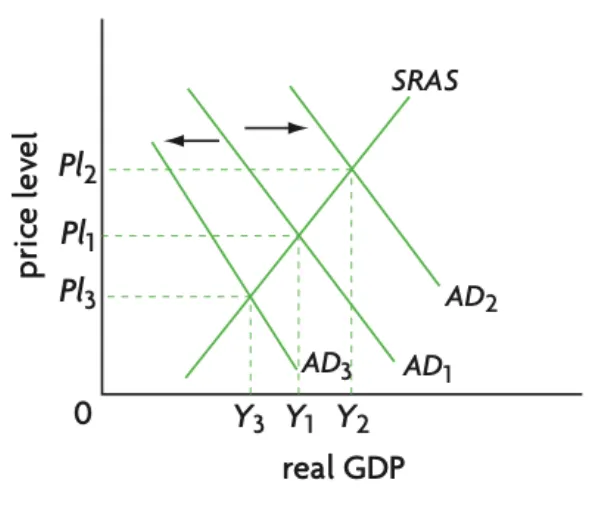

Shifts of the AD curve

Figure 3.2.2 Shifts of the AD curve

•

AD will shift only if the determinant causes a change (increase or decrease) in the components of AD.

•

AD1 → AD2: increase in AD.

•

AD1 → AD3: decrease in AD.

Determinants of AD components

•

Consumption expenditures (C): spending by households on durables and nondurables and services

◦

Interest rates:

▪

Interest rate ↑ → cost of borrowing → C ↓

◦

Consumer confidence:

▪

▪

Confidence ↑ → C ↑

◦

Household wealth:

▪

Wealth ↑ → C ↑

◦

Personal income tax:

▪

Income tax ↑ → disposable income ↑ → C ↓

◦

Household indebtedness:

▪

Indebtedness ↑ → C ↓

◦

Expectations of future price level:

▪

Households expect future price levels ↑ → C ↑

•

Investment expenditures (I): spending by firms on capital goods per period of time.

◦

Interest rates:

▪

Interest rates ↑ → borrowing cost to finance the purchase of capital goods ↑ → I ↓

◦

Business confidence

▪

Confidence ↑ → I ↑

◦

Technology

▪

Fast improvement in technology → I ↑

◦

Business tax

▪

Business tax ↓ → profitability of business projects ↑ → I ↑ .

◦

Corporate indebtedness

▪

Indebtedness ↑ → I ↓

•

Government expenditure (G):

◦

Current spending on goods and services.

◦

Capital spending.

◦

Transfer payments: pension, unemployment benefits.

•

Net exports (X-M): Difference between spending by foreigners on domestic output minus domestic spending on foreign output or difference between export revenues and import expenditures per period of time.

◦

Income of trading partners

incomes of trading partners ↑ → spending on exports ↑ → X-M ↑ →

Exchange rates

•

Trade policies: restrictions to international trade (e.g. tariffs, quotas).

Imposition of tarrif or quota → imports → X-M ↑

Aggregate supply

Aggregate supply(AS): total level of output domestic firms are willing to offer at average price levels per period of time.

AS under the monetarist/new classical model

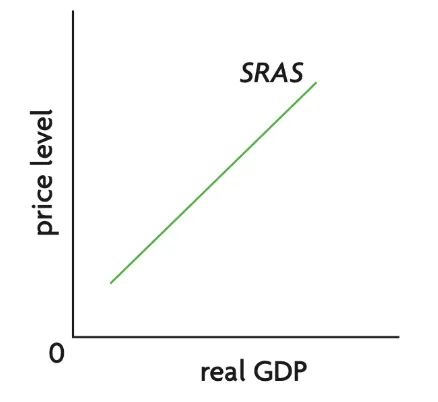

Short-run aggregate supply

Short-run(SR): the period during which money wages are fixed and unable to adjust to changes in the price level.

The shape of the SRAS curve is upward sloping

•

If the average price level (APL) increases, real wage decreases (i.e. wage adjusted to levels of inflation drops), so firms are able to offer more output.

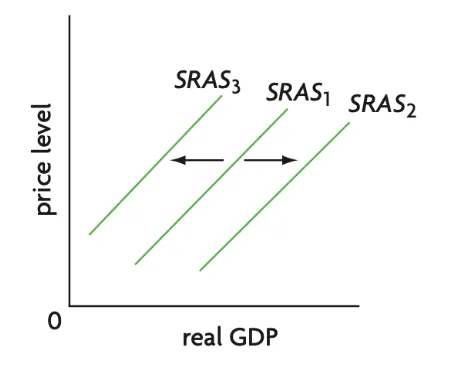

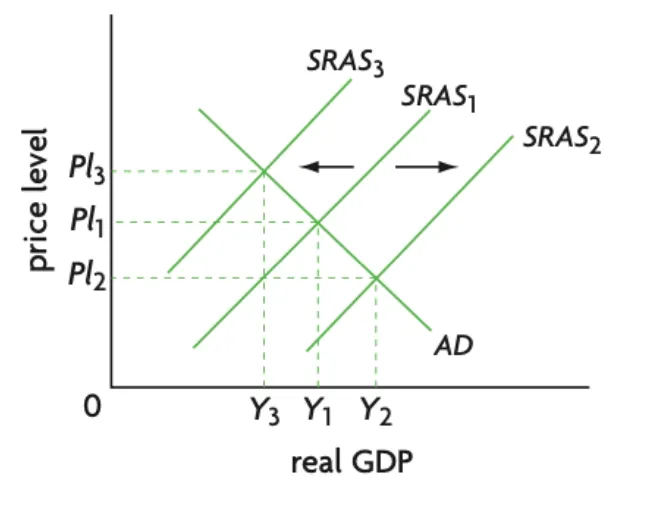

SRAS curve shifts due to:

•

Money wages change - i.e. change in the minimum wage: money wage ↑ → firm’s production cost ↓ → SRAS ↓ → leftward shift of SRAS curve (SRAS1 → SRAS3).

•

Energy price change: oil price change: oil price ↑ → firm’s production cost ↓ → SRAS ↓ → leftward shift of SRAS curve (SRAS1 → SRAS3).

Indirect tax or subsidy change: indirect tax ↑ → cost of production ↑ → SRAS ↓ → leftward shift of SRAS curve (SRAS1 → SRAS3).

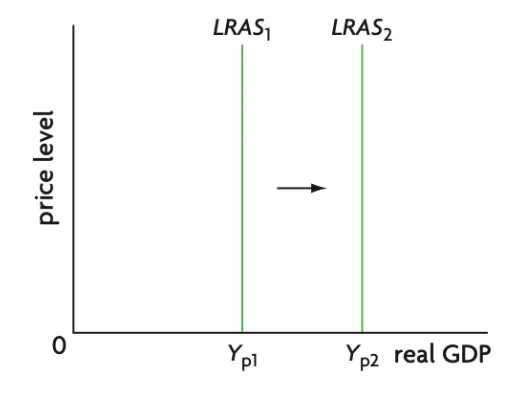

Long-run aggregate supply

Long-run(LR): money wages are assumed to be flexible and able to fully adjust to changes in the price level.

The shape of the LRAS curve is vertical

•

Changes in APL don’t affect real output because real wage is not affected (i.e. wage can fully adjust to changes in the price level).

LRAS curve shifts due to:

•

Change in quality of factors of production: greater education level → quality of labour ↑ → LRAS ↑ → rightward shift of LRAS curve (LRAS → LRAS’).

•

Change in quantity of factors of production: immigration → quantity of labour ↑ → LRAS ↑ → rightward shift of LRAS curve (LRAS → LRAS’).

•

Improvement in technology: technological innovation → improved machines and equipment → able to produce more output → rightward shift of LRAS curve (LRAS → LRAS’).

•

Efficiency ↑ → produces a greater quantity of output → rightward shift of LRAS curve (LRAS → LRAS’).

•

Institutional change - improvements in institutional framework → economy’s productive capacity ↑ → rightward shift of LRAS curve (LRAS → LRAS’).

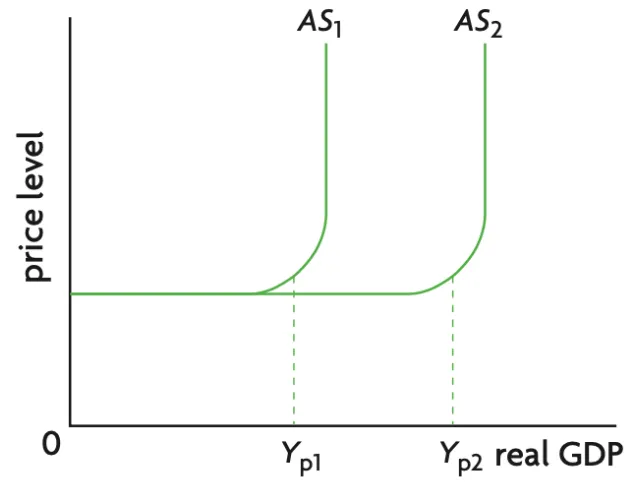

Aggregate supply under the Keynesian model

Figure 3.2.3 Aggregate supply curve (Keynesian)

•

Section I: horizontal - higher levels of output are produced without the average price level (APL) rising.

•

Section II: upward sloping AS curve - some economies may reach full employment faster than others.

•

Section III: vertical at the full employment level of output (Yf) - no unemployment in the economy.

◦

Real output cannot increase beyond Yf.

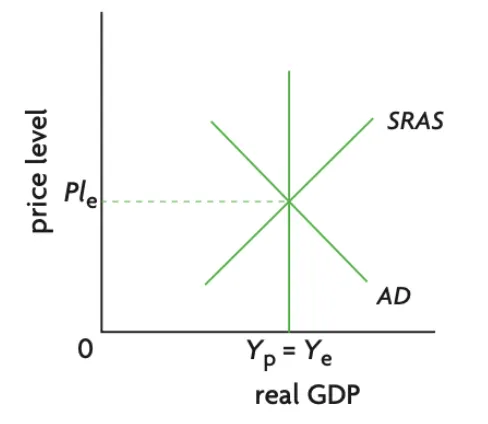

Macroeconomic equilibrium

Equilibrium in the Monetarist / New Classical model

Short-run equilibrium

Exists at the level of output at which AD is equal to SRAS.

A shift in AD → changes the equilibrium average price and output levels in the same direction as the shift in AD.

Shift in SRAS → changes the average price level and output levels in the opposite direction as the shift in SRAS.

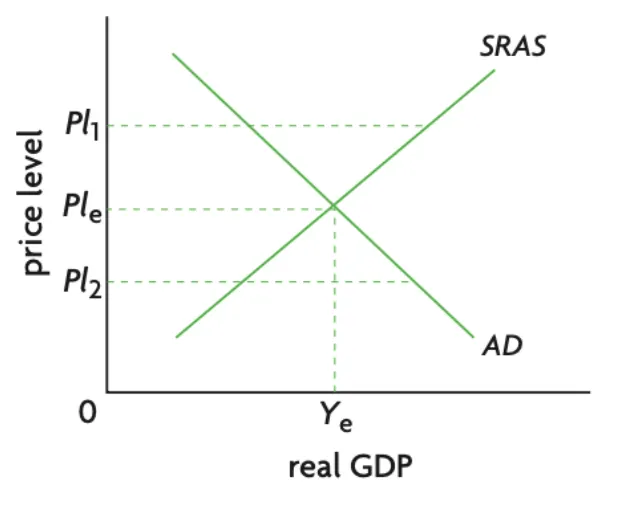

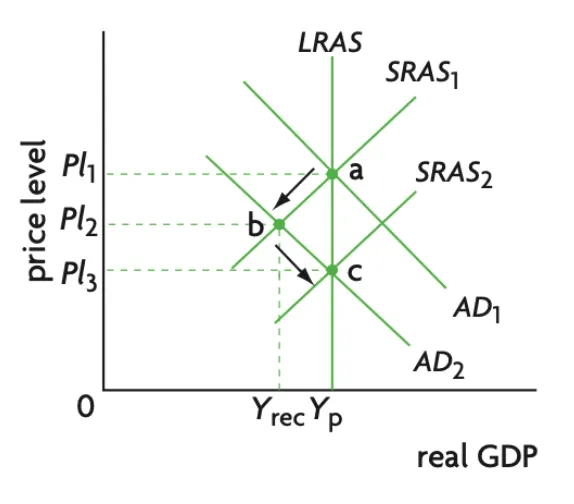

Long-run equilibrium

•

A: real output is at its potential level (Yp), unemployment is at its natural level (NRU), and the average price level is at APL.

•

A→B: business & consumer confidence decrease → consumption & investment expenditure decrease → AD decrease (AD1 → AD2) → average price level decrease (APL1 → APL2).

Deflationary gap (recessionary gap): exists when equilibrium real output is below the potential (full employment) level of output.

Inflationary gap:

exists when equilibrium real output is greater than potential (full employment) output.

•

Money wages are assumed to be flexible in the long run → real wage returns to its original level → unemployment returns to its natural level (NRU) → economy automatically moves to A3.

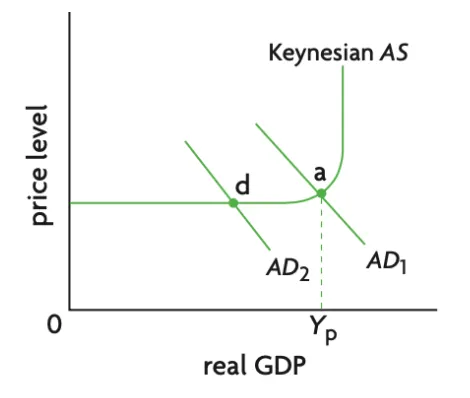

Equilibrium in the Keynesian model

•

Money wages are assumed to be ‘sticky downwards’ - AD is the driving force behind the equilibrium level of economic activity.

Deflationary gap: between Yr2 & Yf

•

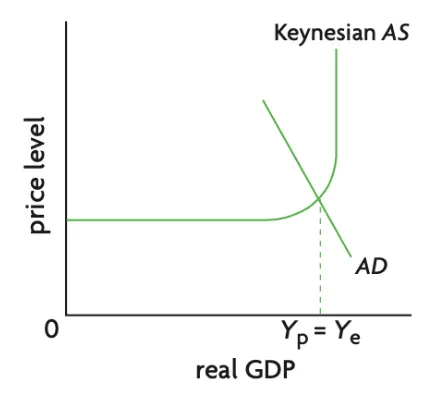

Initial: full employment (Yf).

•

Money wages are ‘sticky downwards’ - i.e. the economy may remain stuck in a deflationary gap.

•

Government must intervene in order to restore full employment.

◦

Expansionary fiscal policy.

◦

Expansionary monetary policy.

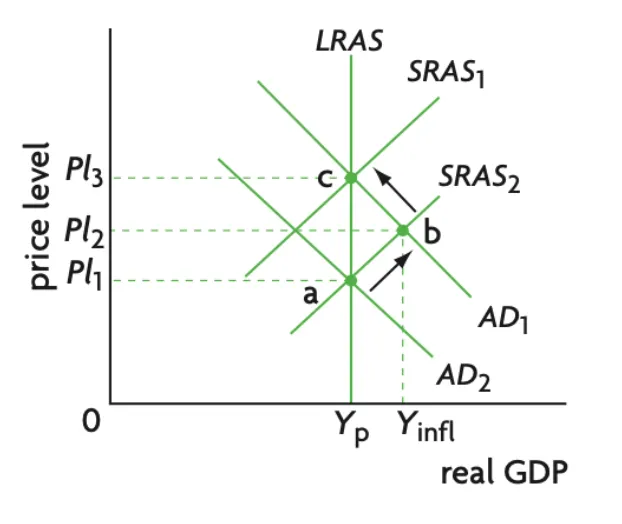

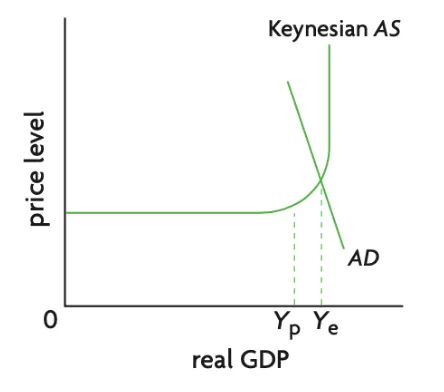

Inflationary gap: vertical distance between a & b

•

Initial: the economy is at full employment level of output Yf

•

Business & consumer confidence ↑ → rightward shift of AD (AD1 → AD2) → equilibrium real output remains at Yf // APL ↑ (APL1 → APL2).

Inflationary gap: between Yfe & Y1

•

Incorporates idea of the natural rate of unemployment.